iyeung144.github.io

My Github Pages

Equity Index Standard Deviation

by Yeung Ka Ming, CFA

Summary

Equity Index (Hang Seng Index of Hong Kong) and Standard Deviation Relationship

R Libraries

library(tidyverse)

library(quantmod)

library(ggplot2)

Preparation of data

Direct download by getSymbols

tickers <- c("^HSI","^GSPC")

getSymbols(Symbols = tickers,

src = "yahoo",

index.class = "POSIXct",

from = "1997-01-01")

## [1] "^HSI" "^GSPC"

Drop the NA and add daily return column, daily standard deviation (SD) and annualised SD

GSPC.new <- na.omit(GSPC)

GSPC.new <- merge(GSPC.new, dailyReturn(GSPC.new$GSPC.Adjusted))

colnames(GSPC.new)[7] <- "GSPC.adj.ret"

GSPC.new <- merge(GSPC.new,rollapply(GSPC.new$GSPC.adj.ret, 252, sd))

colnames(GSPC.new)[8] <- "GSPC.adj.std"

GSPC.new <- merge(GSPC.new, GSPC.new$GSPC.adj.std*sqrt(252))

colnames(GSPC.new)[9] <- "GSPC.adj.std.annualised"

HSI.new <- na.omit(HSI)

HSI.new <- merge(HSI.new, dailyReturn(HSI.new$HSI.Adjusted))

colnames(HSI.new)[7] <- "HSI.adj.ret"

HSI.new <- merge(HSI.new,rollapply(HSI.new$HSI.adj.ret, 252, sd))

colnames(HSI.new)[8] <- "HSI.adj.std"

HSI.new <- merge(HSI.new, HSI.new$HSI.adj.std*sqrt(252))

colnames(HSI.new)[9] <- "HSI.adj.std.annualised"

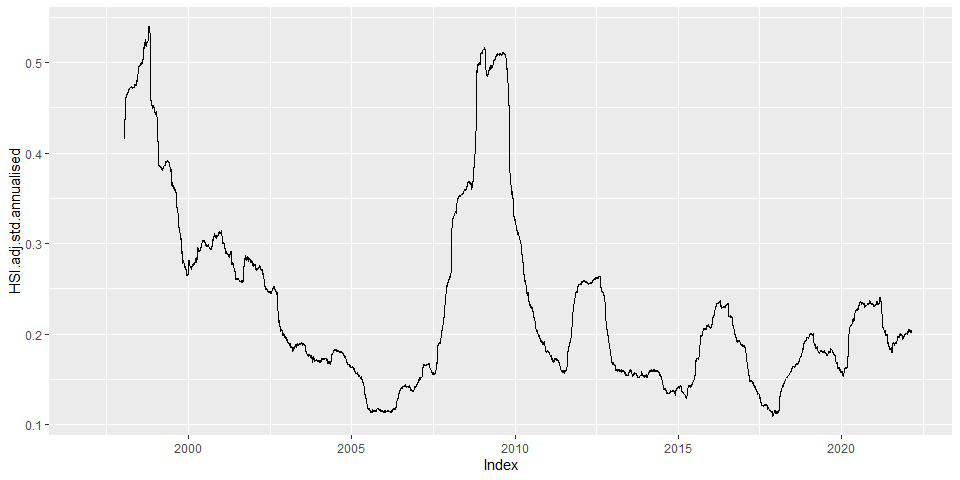

Convert to tibble for easier plotting

HSI.new.tbl <- as_tibble(fortify(HSI.new)) #fortify to keep the datetime index

Plot

p <- ggplot(HSI.new.tbl, aes(x=Index,y=HSI.adj.std.annualised))

p+geom_line()

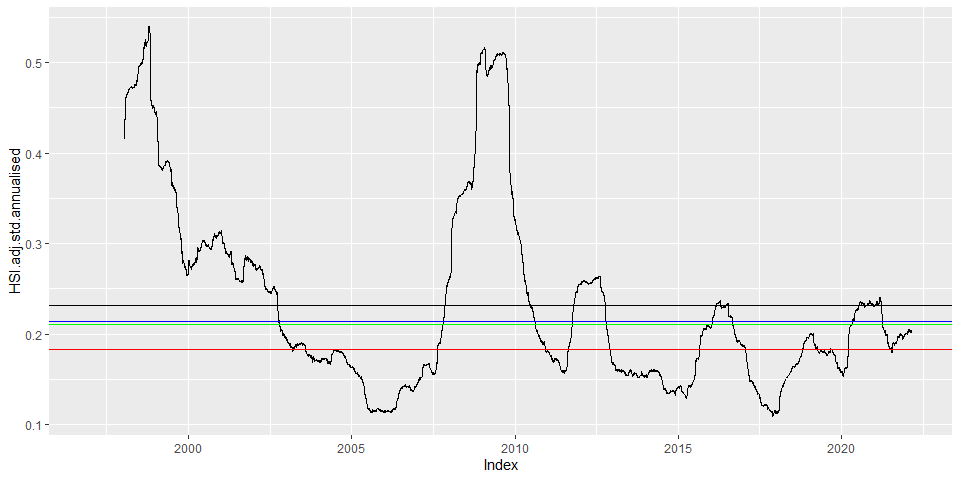

avg10yr <- mean(HSI.new$HSI.adj.std.annualised["2011/2022"])

avg15yr <- mean(HSI.new$HSI.adj.std.annualised["2006/2022"])

avg20yr <- mean(HSI.new$HSI.adj.std.annualised["2001/2022"])

avg25yr <- mean(na.omit(HSI.new$HSI.adj.std.annualised["1997/2022"]))

p+geom_line()+

geom_hline(yintercept = avg10yr, color = "red")+

geom_hline(yintercept = avg15yr, color = "blue")+

geom_hline(yintercept = avg20yr, color = "green")+

geom_hline(yintercept = avg25yr, color = "black")

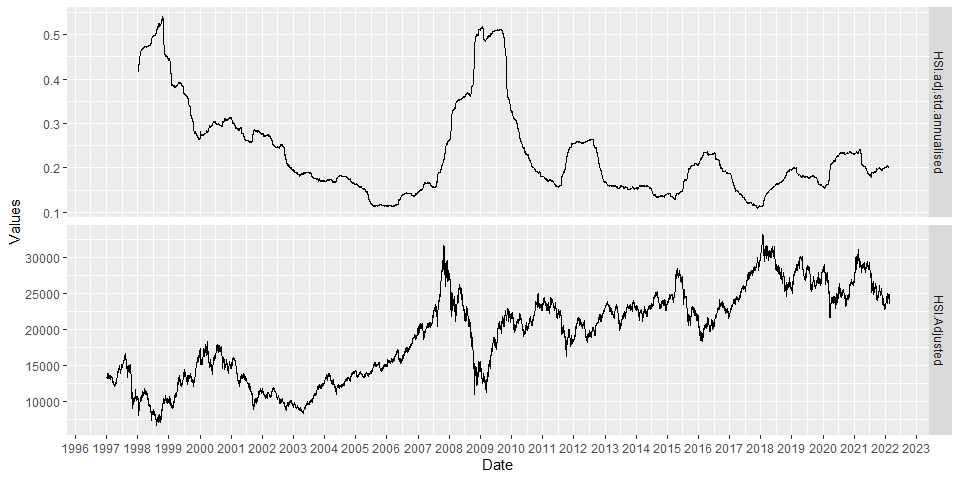

HSI.new2.tbl <- HSI.new.tbl %>%

pivot_longer(cols = c("HSI.Adjusted","HSI.adj.std.annualised"),

names_to ="Series",

values_to = "Values") %>%

select(c(Index,Series,Values))

p1 <- ggplot(HSI.new2.tbl, aes(x=Index,y=Values))

p1 + geom_line() +

facet_grid(Series ~ ., scales = "free") +

scale_x_datetime(name = "Date", date_breaks = "1 year", date_labels = "%Y")